I feel stuck between two different worlds this week. On one hand, there's four-day rally in the stock market. There are almost as many different perspectives on what exactly this upturn means as there are commentators on TV, in the newspapers and online, which is to say thousands all told. I personally don't claim to have anywhere near the amount of knowledge and experience to predict what this means, if anything; I'm simply going to hope for the best and continue to invest my money as regularly, calmly, and automatically as possible.

Now, onto the other world...I am working part-time as an organic chemistry tutor at my old university. There is a test this coming Tuesday, the second of the year. For many of the students, this test could very well determine the course of their future; many of them are trying to get into the Pharmacy school, and if their grades are not good enough, they won't have a chance. Add in the drop course policies, and this is literally the last chance some of them will have to make it into the Pharmacy school.

Why do I bring this up? Simple; for these students, the broader economy is last thing on their mind. By the time they graduate from Pharmacy school in 2013 (if they make it in, of course), this week's financial news might be remembered as a temporary deviation in a horrible market, or as the first coffin nail for the Recession of 2008. And that's assuming it's remembered at all.

Much more importantly, this is yet another reminder of the importance of a long-term perspective. What happens from week to week isn't nearly as important as where you end up. The struggles the students face from one test or even one course are nothing compared to their final degrees. And by the same token, we as investors have to focus on our goals, and not the ups and downs the market throws at us.

Which is why, even though I track my portfolio's progress every week, I do it for my own information and knowledge. Slow and steady wins the race, and makes Roger a wealthy man...

Savings

PNC (Checking Account) $ 185 +$85

Susquehanna (CD) $ 2542 +$0

ING Direct (Checking) $ 105 -$550

ING Direct (Savings) $ 3006 +$0

ING Direct (Orange CD) $ 1016 +$0

HSBC Direct (Savings) $ 23 +$0

Smarty Pig (Savings) $ 700 +$0

Vanguard (Money Market) $ 1301 +$0

Total Savings $ 8878 -$465

Investments

Vanguard (Roth IRA) $ 5526 +$636

- Small Cap Index (NAESX) $ 3159 +$359

- High Dividend Yield (VHDYX) $ 2367 +$277

Share builder (ETFs) $ 2710 +$555

- Total US Market (TMW) $ 895 +$241

- Extended Market (VXF) $ 745 +$99

- Total Foreign (VEU) $ 526 +$101

- Small Cap Value (VBR) $ 249 +$59

- Emerging Markets (VWO) $ 295 +$55

Total Investments $ 8236 +$1191

Total Assets $ 17,114 +$726

Debts

MasterCard (JCPenney) ($ 135) -$28

American Express ($ 1912) -$115

Student Loans ($ 11,866) +$63

Total Debts ($ 13,913) -$80

Net Worth $ 3201 +$646

A rather good week, investment-wise. I will admit to a mild bit of disappointment; if I was still making the same level of investments I was making while I was working, I'd be in an even better position to take advantage of this rebound (if it is in fact a rebound and not a fluke) and make money on the uptick.

But, other than that, things are looking good; investments are doing fine, my Sharebuilder purchases went through alright (three hundred dollars of the increase there is added investment capital), and my spending was kept under control (especially for a weekend I went to visit my girlfriend). All in all, an excellent week.

Saturday, March 14, 2009

Friday, March 13, 2009

Active, Passive, and Portfolio Income: Which is Best?

If you read any financial literature, chances are you've come across the terms active income, passive income, and portfolio income. You might wonder what each of these terms means and which one is the best type of income, especially when it seems that there almost as many recommendations as there are authors. Here's the quick rundown:

Active Income: the income you earn from work you perform. It can either be an hourly wage or an annual salary, depending on the exact position. Generally speaking, if people ask you what you do for a living, you'll respond with your source of active income. Also known as 'earned income'.

Pros: You can make more money initially via active income than you could with passive income (that is, the income from the first month at a new job will be higher than your first month's profit from most passive sources). Also, you can usually raise your active income simply by working longer, which will result in more paid hours or possibly a raise.

Cons: You need to keep working to keep making money; if you quit your job or get fired, your income stream will dry up. (Also, it's been argued that the tax system favors other sources of income, at least here in America; but that depends a lot on your specific situation.)

Passive Income: the money that's earned which doesn't require your material involvement. Common examples are rental income on properties, royalties from books, and blogs (like the one you're reading now). Once the initial work to create them has been completed, the amount of money they earn is independent of the time devoted to them.

Pros: Your income does not depend on the hours of work performed. That is, once the book or website has been created or the rental property purchased, the income can grow independently of the time spent by the owner. As a result, it's possible to earn money in your sleep with such income sources.

Cons: Your income does not depend on the hours of work performed. The nature of passive income is a double-bladed sword. While it's true that you can conceivably earn much more money creating passive income sources than you could with active income, you can also spend time creating a website or buying rental properties that end up returning nothing (or even costing you money).

Portfolio Income: Sometimes considered a sub-section of passive income, portfolio income comes from monetary investments in things like stocks, bonds, and mutual funds. Usually, portfolio income refers more specifically to money generated in the form of dividends, rather than increasing prices (capital gains). Portfolio income involves using your money to make more money, by putting it into vehicles for financial growth.

Pros: Like passive income, portfolio income grows without requiring your involvement. Once you've put your money into a particular investment, the money can grow without you needing to do anything else at all. (Although, watching your investment in case things change is always a good idea.)

Cons: To generate portfolio income, you need money in order to start investing; you'll need another source of income to create your portfolio. Also, as the recent events have shown, there is a lot of volatility in the financial markets, and you have to have back up plans in case your portfolio does not perform as well as expected.

Which type of income is best? The answer to the question is, they all have their own uses as you create a stable financial future. Active income will help you generate seed money that can be put into your portfolio. Your portfolio will grow and build up, enabling you to get more portfolio income out of it. And passive income sources can be cultivated, providing you with supplemental money to put towards your financial goals. Combine the three, and you've got a full and bountiful garden, ideal for creating a solid financial future.

Active Income: the income you earn from work you perform. It can either be an hourly wage or an annual salary, depending on the exact position. Generally speaking, if people ask you what you do for a living, you'll respond with your source of active income. Also known as 'earned income'.

Pros: You can make more money initially via active income than you could with passive income (that is, the income from the first month at a new job will be higher than your first month's profit from most passive sources). Also, you can usually raise your active income simply by working longer, which will result in more paid hours or possibly a raise.

Cons: You need to keep working to keep making money; if you quit your job or get fired, your income stream will dry up. (Also, it's been argued that the tax system favors other sources of income, at least here in America; but that depends a lot on your specific situation.)

Passive Income: the money that's earned which doesn't require your material involvement. Common examples are rental income on properties, royalties from books, and blogs (like the one you're reading now). Once the initial work to create them has been completed, the amount of money they earn is independent of the time devoted to them.

Pros: Your income does not depend on the hours of work performed. That is, once the book or website has been created or the rental property purchased, the income can grow independently of the time spent by the owner. As a result, it's possible to earn money in your sleep with such income sources.

Cons: Your income does not depend on the hours of work performed. The nature of passive income is a double-bladed sword. While it's true that you can conceivably earn much more money creating passive income sources than you could with active income, you can also spend time creating a website or buying rental properties that end up returning nothing (or even costing you money).

Portfolio Income: Sometimes considered a sub-section of passive income, portfolio income comes from monetary investments in things like stocks, bonds, and mutual funds. Usually, portfolio income refers more specifically to money generated in the form of dividends, rather than increasing prices (capital gains). Portfolio income involves using your money to make more money, by putting it into vehicles for financial growth.

Pros: Like passive income, portfolio income grows without requiring your involvement. Once you've put your money into a particular investment, the money can grow without you needing to do anything else at all. (Although, watching your investment in case things change is always a good idea.)

Cons: To generate portfolio income, you need money in order to start investing; you'll need another source of income to create your portfolio. Also, as the recent events have shown, there is a lot of volatility in the financial markets, and you have to have back up plans in case your portfolio does not perform as well as expected.

Which type of income is best? The answer to the question is, they all have their own uses as you create a stable financial future. Active income will help you generate seed money that can be put into your portfolio. Your portfolio will grow and build up, enabling you to get more portfolio income out of it. And passive income sources can be cultivated, providing you with supplemental money to put towards your financial goals. Combine the three, and you've got a full and bountiful garden, ideal for creating a solid financial future.

Thursday, March 12, 2009

Thoughtful Thursday: The Government Is Not Giving You Money

Alas, it seems that everywhere you turn, someone is trying to rip you off. With the recently passed stimulus bill, the scammers, conners, and other rip-off artists have a whole new avenue to abuse. Mrs. Micah reminds us all that the government is NOT going to be sending you a check. (This time around; maybe if we need yet another stimulus in a few months or so...) Be vigilante, be intelligent, and be careful; the best person to watch out for your money is YOU. (Or possibly your mom; but even she can't watch out for you forever.)

Some of the other good posts I've seen in the past week:

How to File Your Taxes for a Recent Graduate - MyLifeROI writes about some of the basics of filing your taxes. He covers several different options, from filing yourself to using professional services, covering the good and bad about each. Personally, given my relatively simple financial situation and low funds, I opted for filing a paper return on my own, but if you have a more complex situation (investments, owning your own business, etc.) you should probably consider professional help.

College Money Tip #12: Free Stuff, Part I - Stephanie of Poorer than You notes several free services that available. She focuses on several budgeting tools, like mint and wesabe as well as some other useful sites. She also mentions NetworthIQ, which I'm particularly interested in (don't be surprised if a little NetworthIQ icon shows up on the side of my blog; as you might be able to tell from my Saturday posts, I like to track how much money I have). Plus, the Part I indicates there will be a Part II coming soon.

I could have kept that $20 (Ethical Quandry) - We heard a story of CleverDude returning money to a confused couple. He raises an interesting ethical question, about what situations we attempt to return money lost by other people, and what lengths we go to do so. Personally, I respect him for making the effort to return the money; ethics are what you do when nobody is forcing you.

Save Money on Television - Lazy Man and Money gives some interesting suggestions on how to save money on your television. The first one I particularly liked, spending more money on your television to save money. Although it's counter intuitive, if you can cut down on the expenses for other entertainment (like going out to the movies) by paying a bit more for television, you'll ultimately save money.

Some of the other good posts I've seen in the past week:

How to File Your Taxes for a Recent Graduate - MyLifeROI writes about some of the basics of filing your taxes. He covers several different options, from filing yourself to using professional services, covering the good and bad about each. Personally, given my relatively simple financial situation and low funds, I opted for filing a paper return on my own, but if you have a more complex situation (investments, owning your own business, etc.) you should probably consider professional help.

College Money Tip #12: Free Stuff, Part I - Stephanie of Poorer than You notes several free services that available. She focuses on several budgeting tools, like mint and wesabe as well as some other useful sites. She also mentions NetworthIQ, which I'm particularly interested in (don't be surprised if a little NetworthIQ icon shows up on the side of my blog; as you might be able to tell from my Saturday posts, I like to track how much money I have). Plus, the Part I indicates there will be a Part II coming soon.

I could have kept that $20 (Ethical Quandry) - We heard a story of CleverDude returning money to a confused couple. He raises an interesting ethical question, about what situations we attempt to return money lost by other people, and what lengths we go to do so. Personally, I respect him for making the effort to return the money; ethics are what you do when nobody is forcing you.

Save Money on Television - Lazy Man and Money gives some interesting suggestions on how to save money on your television. The first one I particularly liked, spending more money on your television to save money. Although it's counter intuitive, if you can cut down on the expenses for other entertainment (like going out to the movies) by paying a bit more for television, you'll ultimately save money.

Lending Club Adventures

As I've been reading more personal finance blogs, I've been coming across the concept of peer to peer (or P2P) lending. One place in particular that's come up multiple times is Lending Club.

I've heard about Lending Club before, but finally decided to take the plunge when I read Stephanie's review of Lending Club on Poorer than You (which, as a side note, is one of the coolest named blogs out there). So, after getting a recommendation link from her, I set out on my merry adventure.

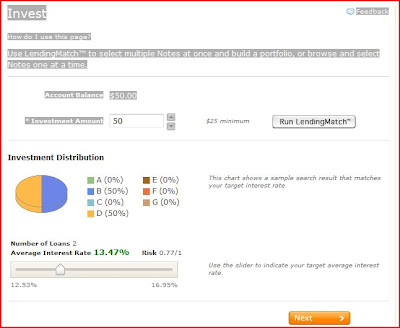

After filling out a few online forms, I was enjoying adjusting the little slider to determine how much risk to take. I came up with a fairly conservative, but still quite profitable arrangement, as shown below:

So, there I was, feeling good about taking this step. I've heard good things about Lending Club, not only from Stephanie but from The Writer's Coin and Rocket Finance. Besides, I had gotten $50 from Lending Club, so it's not like I even had any of my own money on the line.

However; I hit a little snafu...

Apparently, Notes are not currently being sold directly to residents of Pennsylvania. And I happen to be a resident of Pennsylvania, at least when I last checked. As such, I'm not actually allowed to purchase the notes directly. I even went as far as writing to the help desk at Lending Club, which verified that yes, I'm out of luck at the moment.

Interestingly enough, though, there's apparently no rules about buying Notes from other members on their Note Trading platform. (Which perplexes me somewhat; I'd think that if I was not qualified to buy an investment from what is essentially a brokerage house, I should not be able to buy them from other members. It's the same investments, after all; the difference is about the same as buying stocks at an initial public offering versus buying them on a stock exchange.) I'm still trying to study up on the Note Trading platform, and hopefully I'll find some good investments via that method. Prepare for more updates in the near future!

I've heard about Lending Club before, but finally decided to take the plunge when I read Stephanie's review of Lending Club on Poorer than You (which, as a side note, is one of the coolest named blogs out there). So, after getting a recommendation link from her, I set out on my merry adventure.

After filling out a few online forms, I was enjoying adjusting the little slider to determine how much risk to take. I came up with a fairly conservative, but still quite profitable arrangement, as shown below:

So, there I was, feeling good about taking this step. I've heard good things about Lending Club, not only from Stephanie but from The Writer's Coin and Rocket Finance. Besides, I had gotten $50 from Lending Club, so it's not like I even had any of my own money on the line.

However; I hit a little snafu...

Apparently, Notes are not currently being sold directly to residents of Pennsylvania. And I happen to be a resident of Pennsylvania, at least when I last checked. As such, I'm not actually allowed to purchase the notes directly. I even went as far as writing to the help desk at Lending Club, which verified that yes, I'm out of luck at the moment.

Interestingly enough, though, there's apparently no rules about buying Notes from other members on their Note Trading platform. (Which perplexes me somewhat; I'd think that if I was not qualified to buy an investment from what is essentially a brokerage house, I should not be able to buy them from other members. It's the same investments, after all; the difference is about the same as buying stocks at an initial public offering versus buying them on a stock exchange.) I'm still trying to study up on the Note Trading platform, and hopefully I'll find some good investments via that method. Prepare for more updates in the near future!

Wednesday, March 11, 2009

One Million Dollars

The Writer's Coin posited an interesting thought experiment: What would you do with $1,000,000 (after taxes)? It's an interesting idea, as most of us will save for much of our lives to get somewhere near that amount by the time we retire. (Especially adjusting for inflation, since one million now will have the same purchasing power as nearly four million dollars by the time I plan on retiring in about four decades.)

That in mind, here's my 'off the top of my head' answer to what I would do if I woke up tomorrow and found I had inherited one million dollars:

-Tithe ($100,000) - I'm not a terribly religious man (and honestly, I have my doubts about most of the religious 'leaders' in the world, even in my own faith), but I love my church, and I'd want to do what I can to help it out. Plus, given the fact that I'd need a miracle in order to get that much money handed to me, showing some thankfulness is probably in order.

-My Mother ($50,000) - My mother has done so, so much for me over the decades, and the least I can do is try to help her out as she nears retirement, as much as I am able. And I most certainly would be able to help her out if I suddenly had one million dollars to my name.

-A House ($200,000) - Living in my mother's house is not the styling lifestyle I had hoped for in my mid-twenties. Getting a place of my own, preferably near enough to my girlfriend that she can move in with me, is one of my first priorities. I can probably get a nice house near her for this much, or perhaps even less.

-A Diverse Portfolio ($500,000) - The best idea of what to do with a windfall is to put it into investments that can help fund my lifestyle. If I can invest a half million dollars so that it yields about 5% (easily done with an investment of two-thirds stocks and one-third bonds, let's say), that will be $25,000 a year on top of whatever I can earn from work. Although, if I had a million dollars...

-My Dream Career ($150,000) - No, I don't believe that I can buy a perfect career with a few hundred thousand dollars. Rather, this is the money I'd use to live off while I endeavored to live my dream. I can easily get by on less than fifty thousand a year, allowing me to have at least three years to do whatever I want and attempt to build up a career of my dreams.

What career, you ask? Well, if I could be anything I wanted, I'd like to make a living as a professional artist. Which is one good result of this thought experiment; I see that I should be spending more time with my art, hopefully developing my skills more and getting more talented at something I really enjoy.

That in mind, here's my 'off the top of my head' answer to what I would do if I woke up tomorrow and found I had inherited one million dollars:

-Tithe ($100,000) - I'm not a terribly religious man (and honestly, I have my doubts about most of the religious 'leaders' in the world, even in my own faith), but I love my church, and I'd want to do what I can to help it out. Plus, given the fact that I'd need a miracle in order to get that much money handed to me, showing some thankfulness is probably in order.

-My Mother ($50,000) - My mother has done so, so much for me over the decades, and the least I can do is try to help her out as she nears retirement, as much as I am able. And I most certainly would be able to help her out if I suddenly had one million dollars to my name.

-A House ($200,000) - Living in my mother's house is not the styling lifestyle I had hoped for in my mid-twenties. Getting a place of my own, preferably near enough to my girlfriend that she can move in with me, is one of my first priorities. I can probably get a nice house near her for this much, or perhaps even less.

-A Diverse Portfolio ($500,000) - The best idea of what to do with a windfall is to put it into investments that can help fund my lifestyle. If I can invest a half million dollars so that it yields about 5% (easily done with an investment of two-thirds stocks and one-third bonds, let's say), that will be $25,000 a year on top of whatever I can earn from work. Although, if I had a million dollars...

-My Dream Career ($150,000) - No, I don't believe that I can buy a perfect career with a few hundred thousand dollars. Rather, this is the money I'd use to live off while I endeavored to live my dream. I can easily get by on less than fifty thousand a year, allowing me to have at least three years to do whatever I want and attempt to build up a career of my dreams.

What career, you ask? Well, if I could be anything I wanted, I'd like to make a living as a professional artist. Which is one good result of this thought experiment; I see that I should be spending more time with my art, hopefully developing my skills more and getting more talented at something I really enjoy.

Tuesday, March 10, 2009

Investing 101: Stocks

(This is the first entry in a regular series, covering some basic information about a variety of investment options in a question and answer format. It'll be witty, informative, and entertaining, just like high school! Or at least, as what we all wished high school was like.)

Q: What are stocks?

A: In a nutshell, stocks are small ownership portions of a company. If you have Microsoft stock, for example, you are a part owner of the Microsoft corporation.

Q: Sounds good! So, when can I start bossing Bill Gates around?

A: Well, two problems with that: first, Bill is essentially retired, and is putting more time into charity work than Microsoft these days. Second, it's unlikely you own enough stock to have a controlling stake in a company as large as Microsoft.

Q: Well, shoot, that's no fun. What determines how much of the company each share of stock represents?

A: It depends on how much of the company's equity is represented by the stock. If, when initially selling the stock, a company decides to sell 40% of its equity (the value of the company and its assets) in the form of stock, and issues 40,000 shares, then each share will represent 0.001% of the total company. If you bought 1000 shares, for instance,you would own 1% of the total company. Most companies put out millions of stock shares, making it all but impossible for regular investors to gain a controlling (that is, more than 50%) share.

Q: That's interesting. But why should I own stocks?

A: Stocks are good investments as they have high rates of return. They tend to outperform many other investment categories, such as bonds and money market funds, over the long run. They are useful for saving and growing money for people who have time and patience.

Q: That all sounds good, but how exactly can stocks make me money?

A: Stocks have two different ways to return your investment: (a) capital growth: when stock prices rise, you can sell your shares for more money than you used to purchase them, and pocket the profits, and (b) dividends: some (but not all) stocks pay out a portion of the company's profits to shareholders once a quarter, essentially rewarding you for holding onto your shares.

Q: Which of those two methods is best? And how should I invest to achieve that goal?

A: Two questions, hunh? Alright, to answer the first one, it depends on your goals; if you are seeking to grow your money, investing for capital growth should be your aim. If you want to gain spendable money (if you're retired and want a steady source of income), investing for dividends might be better.

You can shift your investments to meet your particular goals. If you want dividends, invest in large, well-established companies (known as blue-chips), which tend to pay out more of their income as dividends. Or invest in REITs, specialized stocks that invest in real estate and are required by law to pay out a large amount of their income. For capital growth, consider investing in smaller companies; they have more room to grow and expand.

Q: That's great! How can I lose?

A: Well, there are risks to owning stocks. Stock prices rise and fall, sometimes dramatically and quickly, so if you can't count on regular capital gains. If the stock prices go low enough, you might even find that the stocks are worth less than the money you paid for them. Dividends can be reduced or even cut entirely, sometimes with little warning. And if a company goes bankrupt, as companies sometimes do, the stock holders are unlikely to get any of their money back; they are behind bond holders and other debtors in claiming corporate assets.

Q: This is getting dicey. How can you find good stocks?

A: That's the $64,000 question; there aren't too many ways to ensure your stocks will do well. The single best method is to do careful, thorough, complete research, completely vetting the companies you want to invest in, and continue to follow the stocks regularly, being sure to know when things change with the company you now (partially) own.

Q: That sounds pretty hard. Is there any way to get the benefits of stocks without all this work?

A: The easiest way is to buy mutual funds. This allows you to own dozens, hundreds, or even thousands of stocks with a single investment. As a result, you'll get the dividends and growth potential of stocks with much less risk, and much less work, than hunting down and studying individual stocks. You will give up the potential of finding a superstar stock that drastically increases in value, but you will avoid the possibility of having a large amount of your money tied up in another Bear Stearns.

That wraps up this week's Investing 101 segment; come back next week, when we'll delve into the wonderful world of bonds.

Q: What are stocks?

A: In a nutshell, stocks are small ownership portions of a company. If you have Microsoft stock, for example, you are a part owner of the Microsoft corporation.

Q: Sounds good! So, when can I start bossing Bill Gates around?

A: Well, two problems with that: first, Bill is essentially retired, and is putting more time into charity work than Microsoft these days. Second, it's unlikely you own enough stock to have a controlling stake in a company as large as Microsoft.

Q: Well, shoot, that's no fun. What determines how much of the company each share of stock represents?

A: It depends on how much of the company's equity is represented by the stock. If, when initially selling the stock, a company decides to sell 40% of its equity (the value of the company and its assets) in the form of stock, and issues 40,000 shares, then each share will represent 0.001% of the total company. If you bought 1000 shares, for instance,you would own 1% of the total company. Most companies put out millions of stock shares, making it all but impossible for regular investors to gain a controlling (that is, more than 50%) share.

Q: That's interesting. But why should I own stocks?

A: Stocks are good investments as they have high rates of return. They tend to outperform many other investment categories, such as bonds and money market funds, over the long run. They are useful for saving and growing money for people who have time and patience.

Q: That all sounds good, but how exactly can stocks make me money?

A: Stocks have two different ways to return your investment: (a) capital growth: when stock prices rise, you can sell your shares for more money than you used to purchase them, and pocket the profits, and (b) dividends: some (but not all) stocks pay out a portion of the company's profits to shareholders once a quarter, essentially rewarding you for holding onto your shares.

Q: Which of those two methods is best? And how should I invest to achieve that goal?

A: Two questions, hunh? Alright, to answer the first one, it depends on your goals; if you are seeking to grow your money, investing for capital growth should be your aim. If you want to gain spendable money (if you're retired and want a steady source of income), investing for dividends might be better.

You can shift your investments to meet your particular goals. If you want dividends, invest in large, well-established companies (known as blue-chips), which tend to pay out more of their income as dividends. Or invest in REITs, specialized stocks that invest in real estate and are required by law to pay out a large amount of their income. For capital growth, consider investing in smaller companies; they have more room to grow and expand.

Q: That's great! How can I lose?

A: Well, there are risks to owning stocks. Stock prices rise and fall, sometimes dramatically and quickly, so if you can't count on regular capital gains. If the stock prices go low enough, you might even find that the stocks are worth less than the money you paid for them. Dividends can be reduced or even cut entirely, sometimes with little warning. And if a company goes bankrupt, as companies sometimes do, the stock holders are unlikely to get any of their money back; they are behind bond holders and other debtors in claiming corporate assets.

Q: This is getting dicey. How can you find good stocks?

A: That's the $64,000 question; there aren't too many ways to ensure your stocks will do well. The single best method is to do careful, thorough, complete research, completely vetting the companies you want to invest in, and continue to follow the stocks regularly, being sure to know when things change with the company you now (partially) own.

Q: That sounds pretty hard. Is there any way to get the benefits of stocks without all this work?

A: The easiest way is to buy mutual funds. This allows you to own dozens, hundreds, or even thousands of stocks with a single investment. As a result, you'll get the dividends and growth potential of stocks with much less risk, and much less work, than hunting down and studying individual stocks. You will give up the potential of finding a superstar stock that drastically increases in value, but you will avoid the possibility of having a large amount of your money tied up in another Bear Stearns.

That wraps up this week's Investing 101 segment; come back next week, when we'll delve into the wonderful world of bonds.

Monday, March 9, 2009

Working Through the Monday Blahs

For those of you who read my post last Monday, you know the college where I am working had Spring Break last week. Since that's currently my only job (although, hopefully not for too much longer *crosses fingers*), I effectively had Spring Break as well. I spent most of it out visiting my girlfriend, and had a great time.

Unfortunately, though, it's left me behind in my blogging. I've managed to get the last two entries out during this rather busy weekend, but I'm getting stuck about what I should write this week. Luckily, I have a few ideas of how to break my mental block:

1) Catch up on my PF blog reading - I've got over two hundred entries to read in my RSS feed, just from the few writers I follow regularly. Reading, digesting, and possibly commenting on all those articles should certainly spark an idea or two.

2) Reading more PF books - I've been falling behind on my reading to learn lately; between my job, my blog, and my personal life, I haven't had a chance to read some of the books I've really wanted to read. Besides sparking some ideas for related posts, it might even be worthwhile to consider putting up a few book reviews.

3) Engage the PF community - I'm currently a member of the Money Blog Network forums, where a lot of PF bloggers gather and discuss various issues. More than a few of the topics I've read through made me think, 'hum, this might make a good blog entry'. Now all I need is some follow through.

4) Write to teach myself - There are plenty of personal finance and money topics I'd like to learn more about; making an effort to identify, study, and then write about those topics would be an excellent learning experience, and would probably provide enough material for years worth of posts.

5) Consider a different blog - I like personal finance, and love writing this blog. But, as they say, variety is the spice of life. Perhaps cutting down on the 7-10 entries a week I put up on this blog and starting another blog for one of my other interests could help to keep me motivated.

Just some thoughts on how to break my Monday 'Blah' mood and start writing again.

Unfortunately, though, it's left me behind in my blogging. I've managed to get the last two entries out during this rather busy weekend, but I'm getting stuck about what I should write this week. Luckily, I have a few ideas of how to break my mental block:

1) Catch up on my PF blog reading - I've got over two hundred entries to read in my RSS feed, just from the few writers I follow regularly. Reading, digesting, and possibly commenting on all those articles should certainly spark an idea or two.

2) Reading more PF books - I've been falling behind on my reading to learn lately; between my job, my blog, and my personal life, I haven't had a chance to read some of the books I've really wanted to read. Besides sparking some ideas for related posts, it might even be worthwhile to consider putting up a few book reviews.

3) Engage the PF community - I'm currently a member of the Money Blog Network forums, where a lot of PF bloggers gather and discuss various issues. More than a few of the topics I've read through made me think, 'hum, this might make a good blog entry'. Now all I need is some follow through.

4) Write to teach myself - There are plenty of personal finance and money topics I'd like to learn more about; making an effort to identify, study, and then write about those topics would be an excellent learning experience, and would probably provide enough material for years worth of posts.

5) Consider a different blog - I like personal finance, and love writing this blog. But, as they say, variety is the spice of life. Perhaps cutting down on the 7-10 entries a week I put up on this blog and starting another blog for one of my other interests could help to keep me motivated.

Just some thoughts on how to break my Monday 'Blah' mood and start writing again.

Sunday, March 8, 2009

PF Spotlight: Punny Money

(Update: As of March 16, Nick and Punny Money have returned. Oh, happy day! His latest post discusses the new Burger King 'burger shots' in his normal sarcastic tone. Check him out, he's still as funny as ever.)

Ah, alas, it is with a heavy heart that I write this particular spotlight. I've wanted to feature one of my favorite blogs, Punny Money, since before I even started this blog. Unfortunately, it seems that Nick, the proprietor of Punny Money, has gone on an unannounced hiatus.

One of the greatest things about Nick's blog is the hilarious cartoons he's been including with his posts. The artwork is fairly simple, largely stick figures and other interesting cartoony aspects. But his twisted sense of humor, and ability to find the funny even in the oddest of places led to some truly, truly funny cartoons. Add in the detailed and insightful articles he wrote, and it's a wonderful blog.

While I hope that Nick will be back to writing and drawing for Punny Money soon, but in the meantime you can check out some of my favorite articles from his blog:

Adventures in First-Time Homebuying - Nick wrote a series of articles about the joy and peril of buying a house. It's easily one of the most comprehensive and complete series of homebuying articles I've seen, covering everything from mortgage rate explanations to finding a realtor to getting a loan and closing. There are over twenty articles in the series, and they make great reading, even if you aren't currently in the market for your first house.

The reason it's the most commented on post is pretty simple; just about everyone has an opinion on the issue of foiling tip inflation. Numerous commentators wrote in to call Nick cheap and paranoid (accusations that weren't helped by the fact that his example had a tip amount of 10%). Angry waiters and waitresses wrote about the number of times that people would give them poor (or nonexistent) tips, and decried the implications that their profession was crooked. Several loyal readers and money nerds commented about how neat the concept was, and expressed their support of the idea. Nothing like raising some controversy to spark an involved conversation.

Ah, alas, it is with a heavy heart that I write this particular spotlight. I've wanted to feature one of my favorite blogs, Punny Money, since before I even started this blog. Unfortunately, it seems that Nick, the proprietor of Punny Money, has gone on an unannounced hiatus.

One of the greatest things about Nick's blog is the hilarious cartoons he's been including with his posts. The artwork is fairly simple, largely stick figures and other interesting cartoony aspects. But his twisted sense of humor, and ability to find the funny even in the oddest of places led to some truly, truly funny cartoons. Add in the detailed and insightful articles he wrote, and it's a wonderful blog.

While I hope that Nick will be back to writing and drawing for Punny Money soon, but in the meantime you can check out some of my favorite articles from his blog:

Adventures in First-Time Homebuying - Nick wrote a series of articles about the joy and peril of buying a house. It's easily one of the most comprehensive and complete series of homebuying articles I've seen, covering everything from mortgage rate explanations to finding a realtor to getting a loan and closing. There are over twenty articles in the series, and they make great reading, even if you aren't currently in the market for your first house.

How to Save Your Safe Deposit Box From All the People Trying to Steal It - Nick details some of the risks of safe deposit boxes, mainly the risk that your bank might declare it abandoned and auction off the contents. He doesn't really come up with a solution (other than putting baking soda labeled as cocaine into your box, so that the police will track you down if your box is declared abandoned...), but the cartoon is hilarious, and the risk of losing your important documents and other deposits is, sadly, real.

Eat Your Money's Worth at Any All-You-Can-Eat Buffet - Exactly what the name says, techniques to maximize the economic benefits of buffet eating. Some of the basics: don't starve yourself, eat the meat first (and second, and third...), and take some time off before you gorge again. Pretty good tips, and useful if you like buffets.

Fight Thieving Restaurants With Checksum Tips - Nick's most commented-on post, it details a method to prevent the wait staff at restaurants from adding more money to the tip than you intended. The basic idea is to make the last digit of the total (the penny column) equal the sum of the dollar digits. So, if your bill (with desired tip) came to about $54.62, you'd add the 5 + 4, and change the last digit to a 9, making the total you actually write $54.69. Then, if anyone tried to add more to the tip, the math wouldn't work, and you'd realize instantly that something was wrong.

Eat Your Money's Worth at Any All-You-Can-Eat Buffet - Exactly what the name says, techniques to maximize the economic benefits of buffet eating. Some of the basics: don't starve yourself, eat the meat first (and second, and third...), and take some time off before you gorge again. Pretty good tips, and useful if you like buffets.

Fight Thieving Restaurants With Checksum Tips - Nick's most commented-on post, it details a method to prevent the wait staff at restaurants from adding more money to the tip than you intended. The basic idea is to make the last digit of the total (the penny column) equal the sum of the dollar digits. So, if your bill (with desired tip) came to about $54.62, you'd add the 5 + 4, and change the last digit to a 9, making the total you actually write $54.69. Then, if anyone tried to add more to the tip, the math wouldn't work, and you'd realize instantly that something was wrong.

The reason it's the most commented on post is pretty simple; just about everyone has an opinion on the issue of foiling tip inflation. Numerous commentators wrote in to call Nick cheap and paranoid (accusations that weren't helped by the fact that his example had a tip amount of 10%). Angry waiters and waitresses wrote about the number of times that people would give them poor (or nonexistent) tips, and decried the implications that their profession was crooked. Several loyal readers and money nerds commented about how neat the concept was, and expressed their support of the idea. Nothing like raising some controversy to spark an involved conversation.

Saturday, March 7, 2009

Weekly Update: 3-7-2009

Well, I have returned from four days spend wining and dining my dear sweet girlfriend Sondra. Actually, the week was pretty slow; other than cleaning up her attic so that she could set up a bedroom/apartment, we were just calm and relaxed. Moving all the necessary furniture and other accouterments up to the third floor was quite an ordeal, but worthwhile to have a place of our own.

Our big fun this trip was going out to see the Watchmen movie. It was very, very good. I've read the graphic novel, and the movie followed the (admittedly complex) storyline rather well. My girlfriend had not read the graphic novel, and she enjoyed it as well. I recommend the movie highly to anyone interested in a smart, deep, action movie.

One caveat though: do not, I repeat, DO NOT take children (or squeamish/prudish friends) to this movie. Although it is a 'comic book movie', it's rather violent (sometimes realistically so) and sexually-charged at times, and the underlying themes and concepts are extremely deep. The best option in my mind is to read the graphic novel first (it's an excellent read) and see if it is appropriate for your family.

Now, to see how my finances are doing after going to visit my girlfriend and spending nearly a week with her:

Savings

PNC (Checking Account) $ 100 -$138

Susquehanna (CD) $ 2542 +$0

ING Direct (Checking) $ 655 +$616

ING Direct (Savings) $ 3006 +$1601

ING Direct (Orange CD) $ 1016 +$4

HSBC Direct (Savings) $ 23 +$1

Smarty Pig (Savings) $ 700 -$1739

Vanguard (Money Market) $ 1301 +$301

Total Savings $ 9343 +$646

Investments

Vanguard (Roth IRA) $ 4890 -$505

- Small Cap Index (NAESX) $ 2800 -$308

- High Dividend Yield (VHDYX) $ 2090 2287 -$197

Share builder (ETFs) $ 2155 -$179

- Total US Market (TMW) $ 654 -$51

- Extended Market (VXF) $ 646 -$66

- Total Foreign (VEU) $ 425 -$27

- Small Cap Value (VBR) $ 190 -$25

- Emerging Markets (VWO) $ 240 -$10

Total Investments $ 7045 -$684

Total Assets $ 16,388 -$38

Credit Cards

MasterCard (JCPenney) ($ 107) -$0

American Express ($ 1797) -$152

Student Loans ($ 11,929) +$0

Total Debts ($ 13,833) -$152

Net Worth $ 2555 -$190

Not a bad week, overall, but not too good, either. Another small hit to my net worth. Another reason to control my spending and bring it under my incoming funds.

Our big fun this trip was going out to see the Watchmen movie. It was very, very good. I've read the graphic novel, and the movie followed the (admittedly complex) storyline rather well. My girlfriend had not read the graphic novel, and she enjoyed it as well. I recommend the movie highly to anyone interested in a smart, deep, action movie.

One caveat though: do not, I repeat, DO NOT take children (or squeamish/prudish friends) to this movie. Although it is a 'comic book movie', it's rather violent (sometimes realistically so) and sexually-charged at times, and the underlying themes and concepts are extremely deep. The best option in my mind is to read the graphic novel first (it's an excellent read) and see if it is appropriate for your family.

Now, to see how my finances are doing after going to visit my girlfriend and spending nearly a week with her:

Savings

PNC (Checking Account) $ 100 -$138

Susquehanna (CD) $ 2542 +$0

ING Direct (Checking) $ 655 +$616

ING Direct (Savings) $ 3006 +$1601

ING Direct (Orange CD) $ 1016 +$4

HSBC Direct (Savings) $ 23 +$1

Smarty Pig (Savings) $ 700 -$1739

Vanguard (Money Market) $ 1301 +$301

Total Savings $ 9343 +$646

Investments

Vanguard (Roth IRA) $ 4890 -$505

- Small Cap Index (NAESX) $ 2800 -$308

- High Dividend Yield (VHDYX) $ 2090 2287 -$197

Share builder (ETFs) $ 2155 -$179

- Total US Market (TMW) $ 654 -$51

- Extended Market (VXF) $ 646 -$66

- Total Foreign (VEU) $ 425 -$27

- Small Cap Value (VBR) $ 190 -$25

- Emerging Markets (VWO) $ 240 -$10

Total Investments $ 7045 -$684

Total Assets $ 16,388 -$38

Credit Cards

MasterCard (JCPenney) ($ 107) -$0

American Express ($ 1797) -$152

Student Loans ($ 11,929) +$0

Total Debts ($ 13,833) -$152

Net Worth $ 2555 -$190

Not a bad week, overall, but not too good, either. Another small hit to my net worth. Another reason to control my spending and bring it under my incoming funds.

Friday, March 6, 2009

Investment Pyramid - Hopes and Goals

Up to this point, we've been talking about the how of investing, from getting yourself ready financially to starting to build up some diverse investments to expanding into other investment opportunities. This is all important to know, but it doesn't touch on the broader question of why we invest. The short answer is, we invest to help us fulfill our hopes and dreams:

The longer answer goes like this: investing gives us more money, and more money (as well as alternative ways to get it) lead to more options. The main reason to invest is that by diverting some of your money from current consumption (that is, not spending all the money you earn), you can help to secure a more stable future.

The money you have, determines the possibilities that are available to you. If you want to retire early (or retire at all), travel the world, engage in philanthropic endeavours, or simply want the flexibility to shift your career without panicking about your income, investing can help you to achieve your goals. There are just a few things to consider as you work toward your goals:

1) Be realistic about your goals - If you're twenty now, making $40,000 a year and don't have any money invested yet, being a millionaire by the age of thirty just isn't realistic. Having $80,000 in investments by thirty is possible, though. Understand what is possible, what's impossible, and how to understand the difference between the two, and you will go far with your investments.

2) Be willing to sacrifice - All investments entail some short-term sacrifice. The money you are putting into stocks or mutual funds could be spent on entertainment now. Being able to say no to going out every night or spending money on a new television is necessary to be a successful investor.

3) Be confident - It's easy to find times when staying in your investments seems risky, or even stupid. As I write this, in March 2009, we are in one of the most volatile markets in decades. It's easy to find people panicking over market volatility, pulling their money out and keeping it in savings accounts or Treasuries.

These actions might make you feel safe in the short term, but it becomes nearly impossible to meet your long term goals with such low growth. Achieving your goals requires taking some (smart) risks, and being confident that investing for the long term will yield positive growth.

With these words of advice, I know you'll do well with your investments. Keep your goals in mind, work towards them every day, and you'll achieve them in the end. Good Luck!

Subscribe to:

Posts (Atom)